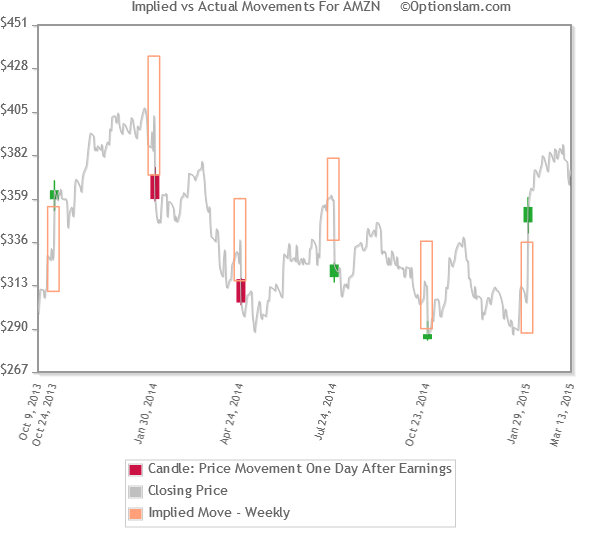

Options pricing gives an indication of what the market expects in stock price range as a result of

upcoming earnings announcement.

With little time remaining to a weekly options expiration, only a small percentage of the extrinsic value can be attributed to true time value.

Therefore, the larger portion of extrinsic value must be associated directly to the markets expectation of the underlying's price range upon the announcement.

At Optionslam, we do of the ATM straddle/strangle to get a handle on what the market thinks the Implied Move will be before and after the earnings.

We also show a history of previous earnings events with the pertinent data highlighting the implied move compared to actual one day move statistics.